Today we get the first of the big jobs data, JOLTS, followed by ADP private sector jobs tomorrow

Outlook

The sudden rise in risk aversion seems to have two causes—first, renewed doubts about AI being such a world-changer and second, a global slowdown that perhaps originates in China and is infecting the world (via Germany). This is the old “China sneezes, Europe catches cold” story and it’s not without some merit.

It’s not clear that the US has to catch a cold. We have some not-hot data in the form of the manufacturing PMI’s, but the labor market data has yet to confirm worries on that front, and in any case, the US economy is the most self-sufficient of the lot.

Today we get the first of the big jobs data, JOLTS, followed by ADP private sector jobs tomorrow and nonfarm payrolls on Friday. In brief, JOLTS is expected to show a drop in openings to 8.10 million from 8.84 million the month before. Treading Economics has a forecast of 8.09, so fractionally worse than the consensus. Of equal or greater interest will be quits and tomorrow’s Challenger job cuts.

Remember that last year, critics complained that the giant job openings number was fake and misleading, with employers coming out of the pandemic with exaggerated qualifications for jobs that nobody could meet. At the same time, the US labor force has some serious problems with obesity, illiteracy and innumeracy, drug addiction and criminal records.

It’s interesting that Trading Economics is feeding the cooling labor market narrative with its ADP forecast, too. Private sector jobs rose by 122,000 and 145,000 is given as the consensus, but Trading Economics has 115,000. We like the Trading Economics fact summaries and charts, but the track record in forecasting is no better than anyone else’s.

Again: on Friday, US payrolls are forecast up by 160-165,000 and the unemployment rate down from 4.3% to 4.2%.

Traders make the mistake of confusing confusion with bad news. Sometimes confusion is just the existence of two seemingly contradictory things at once and patience is needed to clear out the dust. The best example today is the fat rise in nonresidential construction to a record high—see the Key Events above. As WolfStreet says, “Construction spending on manufacturing plants in July, at $19.7 billion, repeated the June record….. The share of spending on factories rose to a record of 19.6% of nonresidential construction spending, having doubled over the past four years. This is now by far the biggest segment of nonresidential construction.”

Sounds good, right? But then Reuters reports JP Morgan has a global manufacturing index that fell to the weakest reading this year. “More concerning are signs that business equipment spending is losing steam – potentially pointing to a weakening in the pace of hiring as well.”

Parsing this out, first note that the Morgan index is a global one, not just the US. Nobody builds factories as a red hot pace without intending to fill them with equipment. Second, manufacturing for only about 10% of the US economy. The Morgan index is not pointing to the US. Export powerhouses Germany and China are the places with a problem.

Canada: The BoC is expected to cut rates today, with perhaps another cut in the pipeline, depending on what chief Macklem says today.

China: Adding to endless speculation about when and how China is going to goose its economy, today the story has it that it will force banks to cut mortgage rates to the tune of $5.3 trillion. Don’t hold your breath.

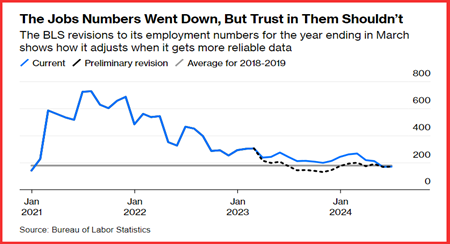

Labor Market Tidbit: Somehow we missed that Sahm has now become a Bloomberg contributor. Yesterday she wrote that the 818,000 revision is no big deal. “In fact, revisions are a normal part of obtaining an accurate picture of the nearly $30 trillion US economy with a labor force of about 170 million people. If the US wants timely statistics — and to limit the burden on survey participants — then revisions are a necessary byproduct.”

Errors not really errors but more likely “incompletes.” Sahm notes “The BLS’s first estimates of monthly payrolls are from a largely voluntary survey of 119,000 businesses and government agencies and come out in just three weeks. This speed comes at a cost. Only about 60% of businesses this year responded in time for the first estimate. The response rate rose to 88% by the third month, but the gap helps explain the early payroll revisions.”

There’s more, but the bottom line is that the BLS has made mistakes, knows it has made mistakes, is working to fix mistakes, and its integrity should not be questioned.

The fact remains that the labor market is cooling. So far it’s nothing to cry about.

Forecast:

We are getting the choppiness we expected. The extra big Sept rate cut expectation is still in play and a little higher than yesterday, which is just the usual foolishness. This probably offers an opportunity to get long the dollar—if you buy the perspective that the labor market did not suddenly fall down a rabbit hole. A little less robust, maybe, but hardly a crisis that would warrant panic behavior by the Fed.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Related

A top recruiter says sports marketing roles are hot right…

Jobs are opening up in the sports industry as teams expand and money flows into the industry.Excel Search &

Public employees and the private job market: Where will fired…

Fired federal workers are looking at what their futures hold. One question that's come up: Can they find similar salaries and benefits in the private sector?

Mortgage and refinance rates today, March 8, 2025: Rates fall…

After two days of increases, mortgage rates are back down again today. According to Zillow, the average 30-year fixed rate has decreased by four basis points t

U.S. economy adds jobs as federal layoffs and rising unemployment…

Julia Coronado: I think it's too early to say that the U.S. is heading to a recession. Certainly, we have seen the U.S. just continue t